GIC Re going public is one of the biggest IPO’s in India’s financial history

Words: Rochelle D’Souza Featured image source: upload.wikimedia.org

{kind=link}

India’s third biggest initial public offering (IPO) is open to subscription. Government run reinsurer General Insurance Corporation of India Limited (GIC Re) has opened its IPO to raise Rs 11,370 crore public money. Earlier this month, GIC Re issued a public notice in which it set a price range of 855-912 rupees per equity share. If fully subscribed at the upper end of the price band, this will be India’s third biggest IPO after Coal India and Reliance Power. This is the first time that the country’s primary market will see public offering by a reinsurer company. According to reports, the government’s move has come to meet the fiscal deficit target of 3.2 percent during the year by divesting some of its stakes in state-run companies.

As per the IPO, the government will sell 107.5 million shares, while the company will raise funds by selling 17.2 million new shares. Banks such as Citi, Axis Capital, Deutsche Bank, HSBC and Kotak are managing the GIC Re IPO. GIC Re has net worth of close to Rs 50,000 crore and total assets of Rs 100,000 crore. The weighted average earning per share (EPS) for 2016-17 is at Rs 32 per share. The estimated market valuation of the corporation, as per the market, will be around Rs 1,00,000 crore. With today’s subscription offerings, GIC could emerge as the top ten most valued public sector companies in India. Malayali business behemoth Alice G Vaidyan is currently GIC’s chairman and managing director.

Image source

{kind=link}

Thought most brokerages have advised investors to go for it, there is a certain level of risk involved while investing in the IPO particularly when one analyses the industry in question. The reinsurance industry is highly competitive and GIC will be in direct competition with a number of worldwide reinsurance companies, many of which have greater financial resources and industry experience. Many a times, foreign currency fluctuations can also reduce net income and capital levels.

Image source

{kind=link}

Here are 10 things you should know before investing in the issue

Strengths of the Company:

- General Insurance Corporation of India is the largest reinsurance company in India with a trusted brand and 44 years of experience. GIC accounted for approximately 60 percent of the premiums ceded by Indian insurers to reinsurers during fiscal 2017 (cited from CRISIL Research) It is also an international reinsurer that underwrote business from 161 countries as of June 30, 2017.

- The IPO, which constitutes 14.22 percent of post-offer paid-up equity share capital, comprises of fresh issue of 1.72 crore equity shares and an offer for sale of 10.75 crore shares by promoter – President of India.

- Bids can be made for minimum 16 equity shares and in multiples of 16 equity shares thereafter.

- GIC intends to utilise net proceeds of the fresh issue towards augmenting the capital base to support growth of business and to maintain current solvency levels; and general corporate purposes. The company will not receive any proceeds from the offer for sale.

- Alice G Vaidyan, the Chairman-cum-Managing Director, has over 30 years of experience in the Indian insurance and reinsurance industry.

Image source

{kind=link}

Risks and Concerns:

- GIC’s success depends upon its ability to accurately assess the risks associated with the businesses that they reinsure, and if actual losses exceed its estimated loss reserves, its net income and capital position will be reduced.

- It operates in a highly-regulated industry and any changes in the regulations or enforcement thereof may adversely affect the manner in which business is carried on and the price of the equity shares.

- There are outstanding litigations against its Corporation, its directors and its group companies and any adverse outcome in any of these litigations may have an adverse impact on its business, results of operations and financial condition.

- Catastrophic events, including natural disasters could materially increase the liabilities for claims and can result in losses and have adverse effect on financial condition and its operations.

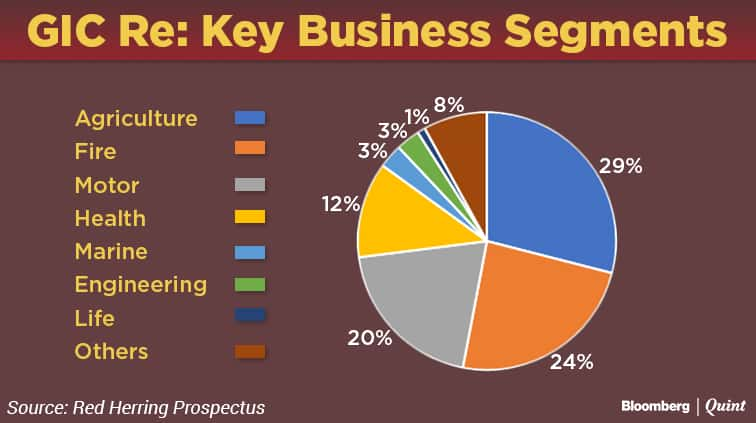

- Substantial increase in their agriculture reinsurance business in recent years exposes them to risks as they have not operated at this level of exposure in agriculture segment before. Particularly, they can face large losses in the event of bad monsoon or successive bad monsoon, drought or flooding.

(With inputs from PTI)